By SHUBHRA JAIN & JAY SANTORO

Knowledge is power. If this adage is true, then the currency of power in the modern world is data. If you look at the evolution of the consumer economy over the past 100 years, you will see a story of data infrastructure adoption, data generation, and then subsequent data monetization. This history is well told by Professors Minna Lami and Mika Pantzar in their paper on ‘The Data Economy’: “Current ‘data citizenship’ is a product of the Internet, social media, and digital devices and the data created in the digitalized life of consumers has become the prime source of economic value formation. The database is the factory of the future.” If we look no further than the so-called big tech companies and distill their business models down in a (likely overly) reductionist fashion: Apple and Microsoft provide infrastructure to get you online, and Facebook (Meta) and Google collect your data, while providing a service you like, and use that data to sell you stuff. Likely none of this is surprising to this audience, but what is surprising is that this playbook has taken so long to run its course in one of the world’s largest and most important sectors: healthcare.

Given the potential impact data access and enablement could have on transforming such a large piece of the economy, the magnitude of the opportunity here is — at face value — fascinating. That said, healthcare is a different beast from many other verticals. Serious questions arise as to whether target venture returns can be extracted in this burgeoning market with the scaled incumbents (both within and outside healthcare) circling the perimeter. Additionally, this is a fragmented ecosystem that has existed (in its infancy) for a few years now with well-funded players now solving for different use cases. Thus, another question emerges as to which areas are best suited for upstarts to capitalize. A key theme in our assessment of the space is that regulation is driving the move towards democratized data access in healthcare, but unlike in regulatory shake-ups of the past, this time start-ups will benefit more than scaled incumbents. Furthermore, we have identified some areas within each approach to this new ecosystem that particularly excite us for net new investment. Let’s dive in.

Why This Time is Different: Regulatory + Market Dynamics

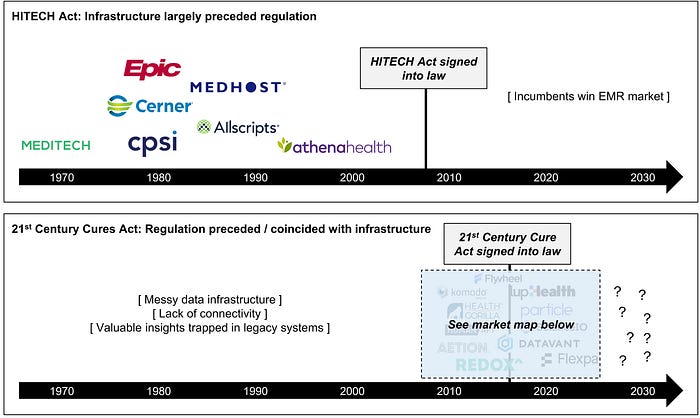

The Health Information Technology for Economic and Clinical Health (HITECH) Act of 2009 brought about an explosion of digital healthcare data by expanding adoption of electronic medical records from ~12% to 96%.

While the primary user of the EMR is the practicing physician in their journey of care delivery, today, there is increasingly demand from other stakeholders in the care ecosystem for the insights that these records hold and hence, the need for a marketplace for this data. Payers want access to the records to help with member population health analytics and risk adjustment. Life sciences companies want access to the records to power real-world data / real-world evidence initiatives for drug discovery and development and patient engagement. Digital health start-ups want access to the records largely to help you manage your specific conditions.

Hiding behind The Health Insurance Portability and Accountability Act of 1996 (HIPAA), EMR vendors and provider organizations have restricted access to this data to retain and entrap the patient base and maintain ownership of a valuable data asset. As of November 2021, at least 70% of healthcare providers still exchange medical information by fax because historically there has been no option to send EMRs using modern internet services.

Even if data sharing is enabled, real challenges persist to accessing longitudinal data for both a patient’s and a population’s health history. While de-identified data can be obtained through business service agreements with data owners and individual patient data can be accessed via consent / permissioned logins to online provider portals, there are few, if any, ways to obtain this data on an aggregated basis across multiple patients and provider organizations. Additionally, challenges to data connectivity, standardization and format integrity exist inside healthcare organizations, which largely house data in disparate internal siloes. As a result, crucial healthcare data that could be used to improve care has been locked in these disconnected, suboptimal record systems.

21st Century Cures Act of 2016 (and related regulations) enabled information sharing, making “sharing electronic health information the expected norm,” thus limiting EMR vendors’ (and other stakeholders’) ability to block the flow of information. A series of related regulations continue to be rolled out to encourage this connected end-state.

The difference this time: at the passing of the HITECH Act, Meditech, Epic, and Cerner had been around for at least 30 years. Hence, these incumbents were well-positioned to fulfill the compliance requirements for the HITECH act and emerged as major winners. As to the proof-points: Meditech approaches half a billion in sales, Epic generated $3.8B in revenue in 2021, and Cerner was acquired for $28B in 2022.

Conversely, in 2016, there were virtually no scaled rails to enable data exchange, integration and sharing in an elegant user interface, especially for stakeholders outside of the provider organizations. In the instance of the 21st Century Cures Act, the rules actually largely pre-dated the required infrastructure.

The question we are exploring is: Will the value created by these rules accrue to scaled incumbents as it did in the wake of the HITECH Act?

Ben Thompson argues in this piece that for consumer/ big tech, this is true. He makes a good case here that today’s cloud and mobile companies — Amazon, Microsoft, Apple, and Google — much like the automotive giants — GM, Ford, and Chrysler — will dominate the market.

There is reason to believe this is possible. After years of seemingly fighting interoperability, the incumbent EMRs are beginning to play ball. As proof-points, Cerner, Allscripts, and athenahealth are founding members of the CommonWell Health Alliance, and Epic is planning to join TEFCA and launched a connection hub to allow any vendor with a connection to Epic to list their app and self-report if they have achieved successful data exchange. Incumbents from outside the healthcare ecosystem (largely from our parallel consumer data story) are swooping in as well. AWS, Google, and Microsoft have all launched healthcare cloud services platforms to help with data normalization and sharing. Apple is offering its HealthKit APIs to help developers access healthcare data for the purpose of creating apps for its iOS and watchOS. Oracle’s acquisition of Cerner is also relevant here by moving healthcare data to the cloud for easy access and sharing.

That said, there is reason to believe these scaled players will struggle. Google, Amazon, and Microsoft have all encountered issues in their pursuit of healthcare profits. While Epic and Cerner have partnered up with big tech (Google and Oracle, respectively) in the wake of the new regulations, early indications show challenges in these relationships.[1] Additionally, the incentive structure for incumbent EHR vendors providing access to the underlying data held by their provider customers is questionable at best. It is also worth noting that, while the duration of the current macro headwinds for the enterprise technology sector is unclear, it is not a stretch to imagine these companies will prioritize their core businesses in the near term. This dynamic, in our view, presents opportunity for upstarts to build both the infrastructure and apps needed for a new era of connected digital health.

Where to Focus / Zooming in: Select Areas of Interest in Healthcare Data

The below captures our take on the current state of play with respect to the different models tackling this problem of healthcare data access.[2] [3]

The above healthcare data category that has (arguably) seen the best outcomes to-date is the net new data generators. These businesses often provide a useful product or service in exchange for rights to and the ability to monetize the underlying data collected. This is not unlike the ad revenue business model in the consumer data economy where consumers are incentivized to contribute their data in exchange for a product/service (often free). For example: Tempus has reportedly raised $1B+ in funding and recently inked pharma deals representing a reported approximately $700M in revenue over the next few years for its combined sequencing + data platform. Evidation has reportedly raised $250M+ in funding around its two-sided consumer-pharma research platform. Perhaps the posterchild of this model, and the entire healthcare data movement, thus far is the oncology-focused Flatiron Health. Flatiron’s OncoEMR is becoming the market leader for oncology practices, plus its others software applications (for example: Flatiron Assist and OncoTrials) are helping make cancer treatment providers much more efficient. In addition, Flatiron delivers data generated at the point of care to help the life sciences community develop new cancer drugs. This is a rare win-win-win: providers no longer have to deal with frustrating technology that is largely from the ’80s, life sciences get access to net new data to improve their drug development, and better outcomes are driven for the patients. This alignment of incentives and creation of a trove of rich, valuable new dataset catalyzed their purchase by Roche for $1.9B.

While the primary data collection strategy is vital to enriching the dataset accessible to the ecosystem, we are at a point where we already have massive troves of data which remain trapped in silos across complex organizations. For example, it is a tedious, largely manual task to extract and integrate our own healthcare data from various hospitals and clinics, oftentimes in multiple states, let alone multiple countries. No scaled player exists today to do this efficiently and digitally for hundreds of thousands of patients, as needed for risk underwriting by payors or real-world initiatives by life sciences companies. The coveted concept of the ‘longitudinal health record’ on either a population (de-identified) or an individual (permissioned) level is still largely ‘on the come.’ The ‘holy grail’ vision is to create an internet of healthcare data that various stakeholders in the healthcare ecosystem can conveniently access for their respective use cases.

This will likely be done piecemeal across various areas, as is the case with the consumer data economy (e.g., there are different companies that get us online, organize our data, and use it to sell relevant services and products to us).

There is an alternative where we achieve a ‘golden mean’ — few new companies seek to simply become systems of record — to store data; rather, they extend the capabilities of existing stores of data — on prem or cloud — and seek to leverage and utilize these data resources in ways that were previously impossible when they couldn’t talk to each other in a fluid, seamless, common language. One of the many ways to achieve and incentivize this shared data ecosystem could be the “give-to-get” model that David Sacks outlines here. Once data sharing becomes the new normal, it will be more interesting to build businesses that can capitalize on this and build high value applications to realize an equitable, accessible, and connected healthcare ecosystem. Just as when cars became a household necessity, building the roads, developing suburbs and selling oil became more interesting.

Footnotes:

[1] Epic did finally ink a commercial deal with Google, but not without Epic putting its customers in the middle of integration disputes and Google almost dismantling its Health unit and laying off hundreds of employees in its Verily Life Sciences unit.

[2] Veradigm also has access to primary data they generate via their family of EHR systems (e.g. PracticeFusion).

[3] Many of these businesses also offer other products and services not captured in this map. For example, Change Healthcare, which sold to Optum in 2022 for $7.8B, primarily offers RCM/payments and imaging solutions.

Shubrha Jain MD, MBA is Head of Healthcare Investments and Jay Santoro is an Associate at Tarsadia Investments, a $2bn fund. This article first appeared on their Medium channel

https://thehealthcareblog.com/wp-content/uploads/2023/05/Jay.jpg

2023-05-19 08:37:00